Hi there!

Welcome to FinSoar. To kick off the new year, I’m analysing the dollar’s — terrible — year, a confused labor market, and the current AI news:

The Dollar's Worst Year in a Decade: And 2026 Looks Worse

The dollar slumped 9.5% against major currencies in 2025, its steepest annual drop since 2017. The euro surged 13.5%, the pound jumped 7.7%, and the Swiss franc climbed 13.9%. "This has been one of the worst years for dollar performance in the history of free-floating exchange rates," said George Saravelos at Deutsche Bank. Trump's tariff chaos in April sparked the initial selloff. The Fed's rate cuts starting in September kept pressure on. Worries about US fiscal deficits, global trade wars, and concerns about Fed independence took a toll. Don't expect relief in 2026. Wall Street banks predict the euro will strengthen to $1.20 by year-end, and the pound to $1.36. The Fed will likely cut rates two more times while the ECB holds or even raises. Trump is expected to announce his Fed chair pick this month to replace Jerome Powell. Kevin Hassett is the betting favorite. Investors are bracing for Trump's pick to be more dovish and cut rates, as the president has repeatedly criticized Powell for not lowering borrowing costs more swiftly. Here's the bigger issue: despite the decline, the dollar remains overvalued. The real broad effective exchange rate stood at 108.7 in October, down only slightly from a record 115.1 in January. "The reality is we still do have an over-valued US dollar from a fundamental standpoint," said Karl Schamotta at Corpay. Trump's attacks on institutions are eroding the foundation of dollar dominance: trust. His sweeping tariffs, undermining of the Fed, and attacks on US agencies question Washington's commitment to the liberal economic order. Surging US debt and persistent deficits of around 6% of GDP add to doubts. Foreign investors have started hedging their dollar exposure when buying US stocks, something they didn't do during the years of unquestioned American dominance. Countries are diversifying reserves into gold, and regional payment systems are proliferating. For investors in the US, it's time to gain more exposure to international markets, especially with the chance of currency appreciation, relative to the US dollar. A weaker dollar boosts US exports by making goods cheaper for foreign buyers, which lead to more tax revenue generation. It also helps multinational earnings by increasing the value of overseas revenues. But it raises import prices and makes European vacations more expensive. The dollar's dominance won't vanish overnight. But the world is entering a financial interregnum where the old order is fading. The second Trump administration may be the catalyst that turns long-running dissatisfaction into systemic change. |

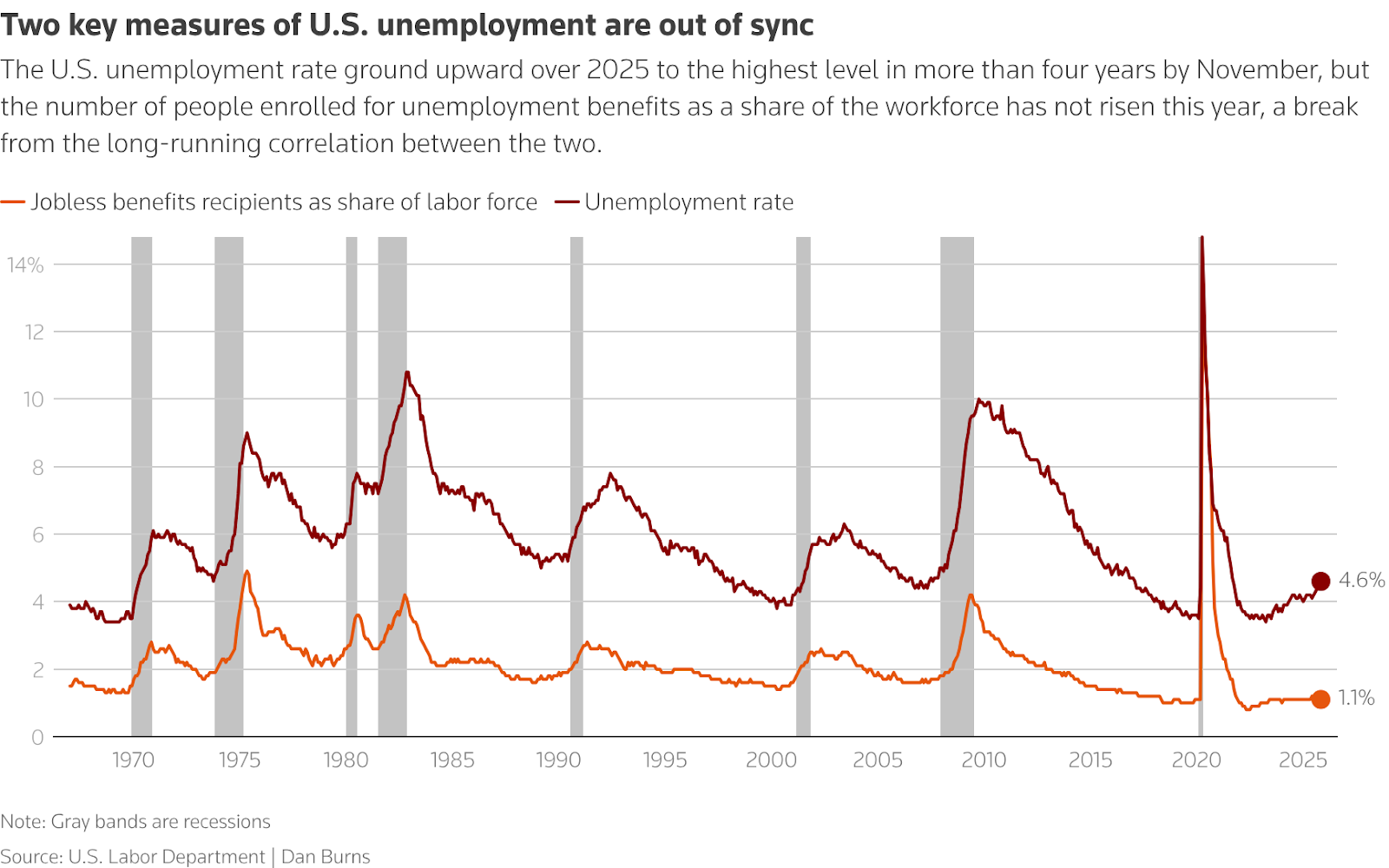

America's Stalled Labor Market

New unemployment claims fell to 199,000 in the week ending December 27, down from 215,000 the prior week. Sounds healthy. But initial jobless claims have fluctuated between 200,000 and 250,000 a week for most of 2025, as employers held onto existing staff in the face of a hazy economic outlook. The labor market remains locked in what economists describe as a "no hire, no fire" mode. While continuing claims eased from recent highs, they remain higher than last year. Hiring has slowed substantially in 2025, averaging just 55,000 new jobs created a month through November, roughly a third of the 2024 pace. The unemployment rate increased to a four-year high of 4.6% in November. Labor demand and supply have been impacted by Trump's steep import tariffs and aggressive immigration crackdown that has limited worker supply, economists say. The slow hiring pace has brought job creation near what economists estimate is the break-even rate that keeps the jobless rate from rising. The surface stability masks deeper problems. The number of Americans on jobless benefits rolls as a share of the labor force is just 1.1% and has changed little, even as the formal unemployment rate climbed from 3.7% in January to 4.6% in November. The lack of correlation between these data points is very unusual, and stands as evidence of reluctance among employers to cut headcount in an environment of still-tight labor supply. The breadth of hiring has narrowed as employers await greater clarity on Trump's policies and gauge workforce needs against the rapid rollout of productivity-enhancing artificial intelligence tools. For the Fed, this creates a dilemma. The unusual attributes of the current job market are central to the debate about whether to cut rates further to forestall employment weakening or hold steady to keep pressure on inflation. Even some policymakers who supported the December rate cut acknowledged "the decision was finely balanced." The labor market isn't collapsing. It's paralyzed. Companies won't hire. They won't fire either. And nobody knows when the freeze ends. If you thought that was all, you should closely investigate workforce dynamics and demographics. Between February and July, Black women lost 319,000 jobs while white men gained 365,000. Roughly 300,000 Black women left the workforce during the first half of 2025, a shift analysts point to as revealing growing structural instability. Proprietary analysis of BLS household data shows Black women's unemployment rate spiked 21 times faster than white men's. The forced exit of Black women from the workforce cost the US $9.2 billion in GDP in 2025. The displacement from stable federal and professional roles into service work is eroding the economic standing of breadwinners in 52% of Black households with children. This wasn't broad economic weakness. This divergence is not a statistical anomaly; it is the mathematical result of policy.

The damage extends beyond Black women. Workers over 40 bore a disproportionate share of labor market disruption. Once displaced, workers over 40 are significantly less likely to be rehired quickly and more likely to stop actively seeking work. Women experienced sharper employment declines and slower recovery than men, particularly in sectors affected by federal cuts, public administration, education, healthcare support and administrative functions. Employment and labor-force participation data show declines for women over the course of the year, alongside rising unemployment relative to late 2024. AI accelerated the damage for early-career workers. Stanford Digital Economy Lab research found workers ages 22-25 in AI-exposed occupations like software development and customer service experienced employment declines of 6% to 13%. Meanwhile, analysis shows a massive 909,000-person jump in involuntary part-time work. Consumer credit reporting data shows an almost 2x increase in consumers using Buy Now, Pay Later services for groceries in a single year. Trump claimed in December that "100 percent of all net job creation has gone to American-born citizens." The administration said 2.57 million US-born citizens obtained jobs in 2025 while about 1 million immigrants lost work. Economists on both sides of the political aisle say they have seen no evidence that American-born workers are getting jobs by the millions. Data shows US-born workers are doing moderately worse under Trump than under Biden because the labor market has weakened. The Trump administration's claims are based on census data that economists warn against using for counts. The census data was hemmed in by a population estimate set in January, before any new immigration policy took effect. When monthly responses from foreign-born households drop, the math takes over: native-born population totals automatically increase. Any drop in foreign-born workers artificially boosts the number of native-born workers reported. Using counts of native-born workers from census population estimates would be "a multiple-count data felony," wrote economist Jed Kolko. The real measure of how US-born workers are doing is the unemployment rate. The unemployment rate for native-born Americans is 4.3%, up from 3.9% last November. "We know that it's just been harder for native-born workers to find work because more of them are unemployed," said economist Stan Veuger. There is little evidence that millions of US-born workers rushed into jobs typically worked by immigrants. The rising unemployment rate for native-born workers indicates that native-born Americans are not moving in large numbers into those jobs. Research on construction shows that the deportation of immigrants in lower-skilled positions can lead to the disappearance of work for native-born construction workers in higher-skilled jobs. "A lot of immigrants take low-wage jobs on projects that wouldn't otherwise go forward," said economist Dean Baker. "When the immigrants aren't there, native-born workers in higher-skilled jobs aren't able to do it." |

Oracle's $300 Billion OpenAI Bet: The AI Trade's Canary in the Coal Mine

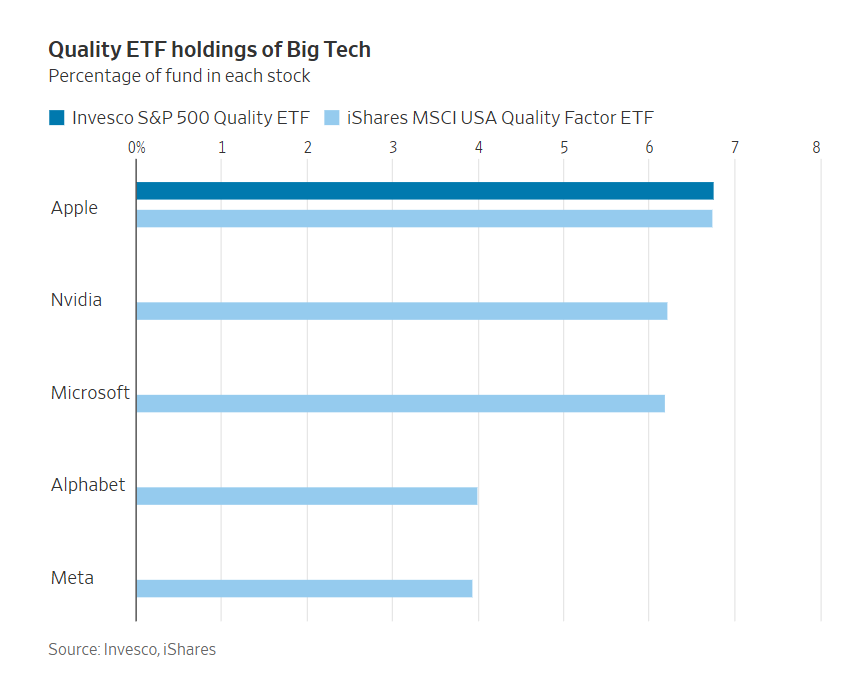

Oracle surged 40% in a single day after its September 9 earnings report, reaching a near-100% gain for the year. Then it all disappeared. By year-end, Oracle's stock fell even lower than before the September report, finishing up just 19.6%. The September surge came from Oracle disclosing $455 billion in remaining performance obligations for its cloud unit, future revenue already under contract. That number later increased to $523 billion. Given Oracle's cloud revenue run rate of just $16 billion, the implication was explosive growth. Then came the sobering detail: $300 billion of that $455 billion came from one company: OpenAI. OpenAI is incurring tens of billions in losses, with recent estimates placing Q3 losses at $11.5 billion and $25 billion over the first three quarters of 2025. OpenAI signed up for $1.4 trillion in future spending commitments. Oracle's $300 billion is just 21%. Oracle is funding the buildout with debt, increasing from $96 billion to nearly $130 billion. Free cash flow flipped to negative $10 billion last quarter. When fully ramped, Oracle expects AI commitments to generate 30-40% gross margins, lower than traditional cloud computing. The cost to insure Oracle's debt against default rose to a 16-year high in December at 1.41%, the highest since the 2009 financial crisis. Michael Burry of "Big Short" fame revealed bets against Nvidia and Palantir on November 3, about $10 million in put options that could amount to more than $1 billion if the stocks drop significantly. His bet pays off if Nvidia falls 37% to $110 by 2027. It's trading around $190 now. Burry focused on Nvidia helping fund customer purchases in deals resembling how Enron financially supported vendors, and accounting around chip life expectancy that could inflate earnings. Nvidia denied Burry's analysis, calling its business "economically sound" with "complete and transparent" reporting. Quality ETFs are dropping AI stocks due to rising accruals. Invesco's $15 billion S&P 500 Quality ETF dropped Nvidia and Meta in June and Microsoft in December. In Nvidia's latest quarter, accounts receivable leapt $16 billion to $33 billion, while accounts payable rose only $3 billion to $8 billion. The gap must be funded while waiting to be paid. "Big Tech companies are pouring hundreds of billions into AI without a clear path to profit, eating into cash and increasingly needing borrowing," the WSJ noted. Yet the first trading day of 2026 looked like 2025, with tech leading. Nvidia and Alphabet advanced more than 1% each, semiconductors rose as a group. The situation is more than odd. Quality funds flee AI stocks. Short sellers position for collapse. And investors keep buying… |

That’s all for today!