Hi there!

Welcome to FinSoar. Workers fears more AI layoffs after Block fires 4,000 employees, Netflix walks away from the Warner Bros. bid, and Mortgage rates drop below 6%:

Block Fires 4,000 Workers, Blames AI, Stock Surges 24%

Block cut 4,000 jobs Thursday, nearly 40% of its workforce, citing artificial intelligence as the reason. CEO Jack Dorsey said "intelligence tools have changed what it means to build and run a company" and predicted most companies will make similar cuts within a year. The stock jumped 24% in after-hours trading. The layoffs came alongside strong Q4 results. Block posted adjusted EPS of $0.65, meeting expectations, while gross profit surged 24% to $2.87 billion. The company raised 2026 guidance, projecting $12.2 billion in gross profit and adjusted EPS of $3.66, well above the $3.22 consensus. Dorsey said "something happened in December" when AI models became dramatically more capable. He told shareholders a "significantly smaller team, using the tools we're building, can do more and do it better" and that capabilities are "compounding faster every week." The CEO chose one massive cut over gradual reductions, saying "repeated rounds of cuts are destructive to morale." Severance includes 20 weeks of base pay plus tenure bonuses, equity vested through May, six months of healthcare and $5,000 cash. Block expects $450 million to $500 million in restructuring charges. The market reaction concerned analysts. CNBC's Steve Sedgwick called it potentially "the biggest story of a tumultuous week," warning it establishes "a clear, public incentive: fire your people, replace them with AI and the market will reward you handsomely." Evercore called the layoffs "a seminal moment" in the AI era. Block had 10,205 employees at year-end 2025, up from 5,477 in 2020 and 3,835 in 2019. Dorsey later acknowledged Block "over-hired during COVID" and built two separate company structures for Square and Cash App instead of one. But he said blaming layoffs on overstaffing "misses all the complexity" including lending, banking and buy-now-pay-later services. Former Block data analyst Ivan Ureña-Valdes, who survived three prior rounds of layoffs, told Business Insider he saw AI automating his work. "So much of the data analyst world is finding the right dataset, writing something that will allow you to pull the data set that you want, and then generating output. Every single one of those steps is significantly faster and easier because of AI." Dorsey said "I don't think we're early to this realization. I think most companies are late." |

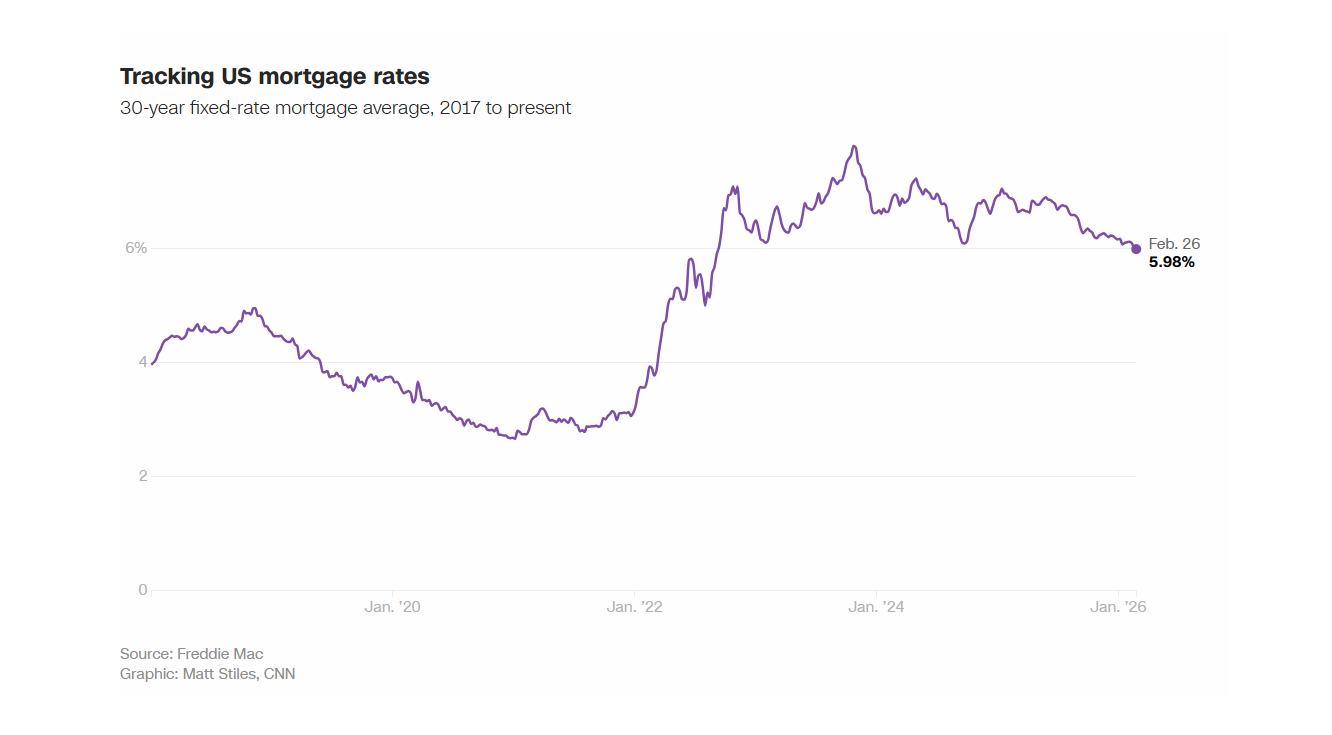

Mortgage Rates Drop Below 6% But Housing Market Stays Frozen

The average 30-year fixed mortgage rate fell to 5.98% this week, the lowest since September 2022. It marks the first time rates have cracked the psychologically important 6% threshold in more than three years, but economists remain skeptical the decline alone will thaw a housing market stuck at 30-year lows. The drop came amid market volatility following the Supreme Court's tariff ruling, not fundamental economic improvement. Trump announced a 15% global tariff over the weekend, sparking a flight to safety that pushed Treasury yields lower. The 10-year yield fell to around 4%, bringing mortgage rates down with it. Rates peaked at 7.8% in October 2023. They averaged 6.76% in February 2025. The improvement translates to real purchasing power. A median-income household can now afford a $331,483 home, roughly $30,000 more than a year ago. The monthly payment on a $400,000 home dropped to $1,916 from $2,105, a difference of $189. But the improvement may not matter much. Supply constraints continue to strangle the market. Nearly 69% of US homes with outstanding mortgages have rates at or below 5%, creating a powerful lock-in effect. About seven out of 10 borrowers are locked into rates below 5%, according to Intercontinental Exchange. Refinancing has surged. Applications are about 130% higher than a year ago. But purchase applications remain weak, just 8% higher year-over-year in mid-February. Existing home sales fell 8.4% in January, the biggest monthly drop in nearly four years. The median home price hit $405,000, up more than 50% since 2019. Rising insurance costs, property taxes and electricity bills add to the burden. Home Depot CFO Richard McPhail said "we have not yet seen a catalyst for an inflection in housing activity." Trump ordered mortgage giants Freddie Mac and Fannie Mae to purchase $200 billion in mortgage bonds last month. Fed minutes noted the purchases caused mortgage-backed securities yields to decline but were "unlikely to materially boost mortgage refinancing" because current rates remain well above existing mortgages. |

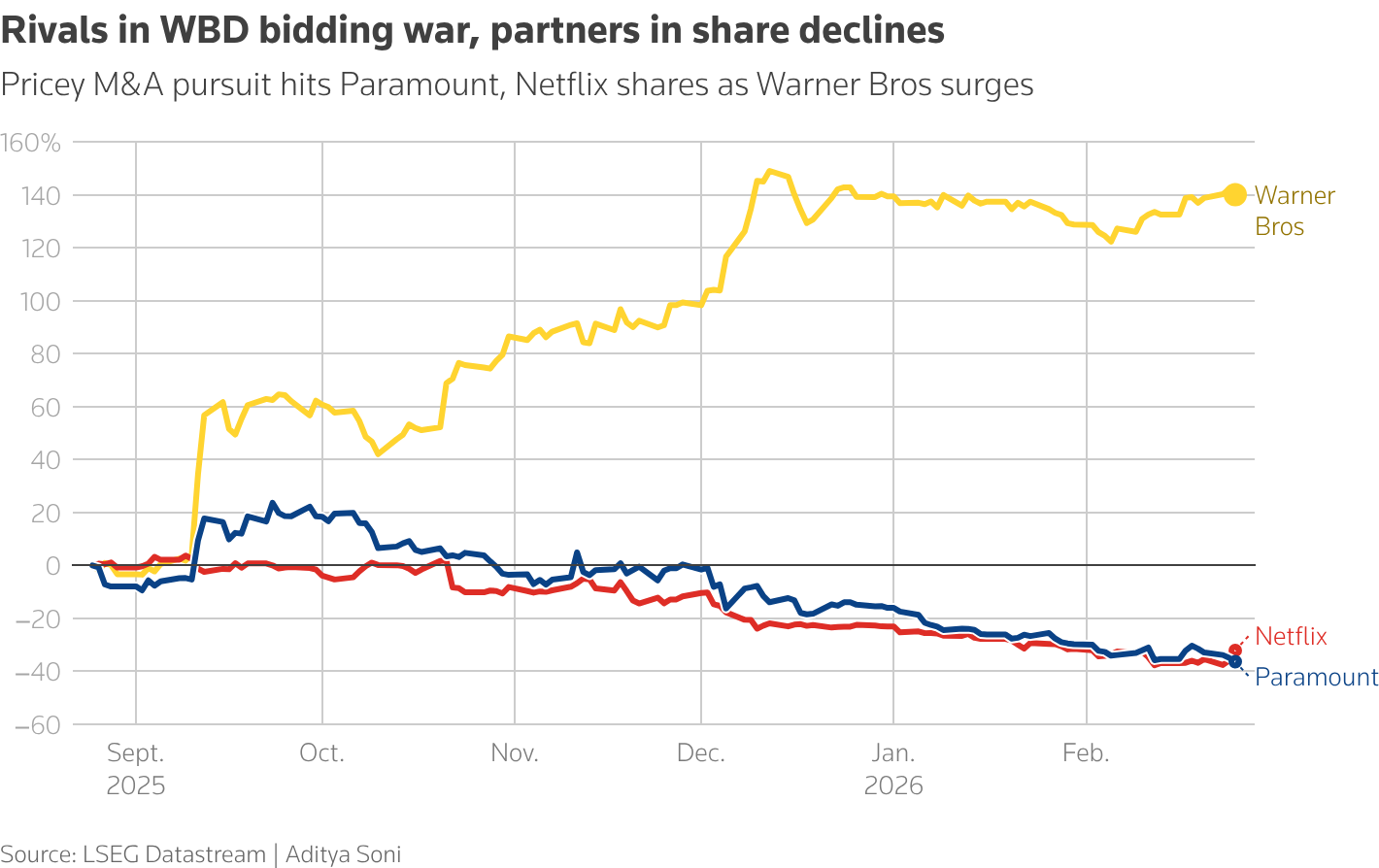

Netflix Walks Away, Paramount Wins $111 Billion Warner Bros

Netflix backed out Thursday of its deal to buy Warner Bros Discovery after the Hollywood studio declared Paramount Skydance's $111 billion bid "superior" to Netflix's offer. The streaming giant refused to raise its price, saying "the deal is no longer financially attractive." Paramount offered $31 per share in cash for the entire company, up from $30 and well above Netflix's $27.75 per share December agreement worth $82.7 billion for just the studio and streaming assets. Paramount's bid includes CNN and cable networks. Netflix's did not. The victory caps a months-long fight where Paramount relentlessly pursued Warner Bros despite repeated rejections. After Warner Bros signed with Netflix in December, Paramount launched a hostile campaign, threatening a proxy fight and continually tweaking terms. The studio finally lured Warner Bros back to the table last week. Paramount sweetened the deal with aggressive protections: a $7 billion breakup fee if regulators block it, agreement to pay the $2.8 billion termination fee Warner Bros owes Netflix, and a quarterly "ticking fee" of 25 cents per share if closing drags past fall. The bid is backed by roughly $45.7 billion in equity and over $57 billion in debt, with financing largely guaranteed by Oracle billionaire Larry Ellison. Markets celebrated. Netflix shares jumped more than 9% Friday as investors cheered the exit from what many viewed as an expensive misfit. Paramount rose about 10%. Warner Bros shares were marginally lower. The deal faces significant regulatory hurdles. California Attorney General Rob Bonta said the merger "is not a done deal" and vowed "vigorous" review. It needs DOJ and European approval. Senator Elizabeth Warren called it "an antitrust disaster threatening higher prices and fewer choices." Politics loom large. The Ellisons are close to Trump, who has attacked CNN repeatedly and said in December it should be sold. Netflix co-CEO Ted Sarandos visited the White House Thursday, meeting with Attorney General Pam Bondi hours before pulling out. Trump called on Netflix to fire board member Susan Rice over political comments. If approved, Paramount would control Warner Bros, HBO, CNN, Food Network and traditional networks including CBS, Nickelodeon and Comedy Central. The combined entity would rival Disney and Comcast's NBCUniversal in scale. |

That’s all for today!