Welcome back to FinSoar!

This week, the stories I bring to your inbox are all connected to each other by the gap between what investors are being asked to believe versus the reality presented by numbers.

The medicare advantage rate hike handed health insurers a lifeline, SpaceX filed for the largest IPO in history, and markets are running out of patience for Tesla…

A $13 Billion Rate Hike Just Rescued Health Insurer Stocks

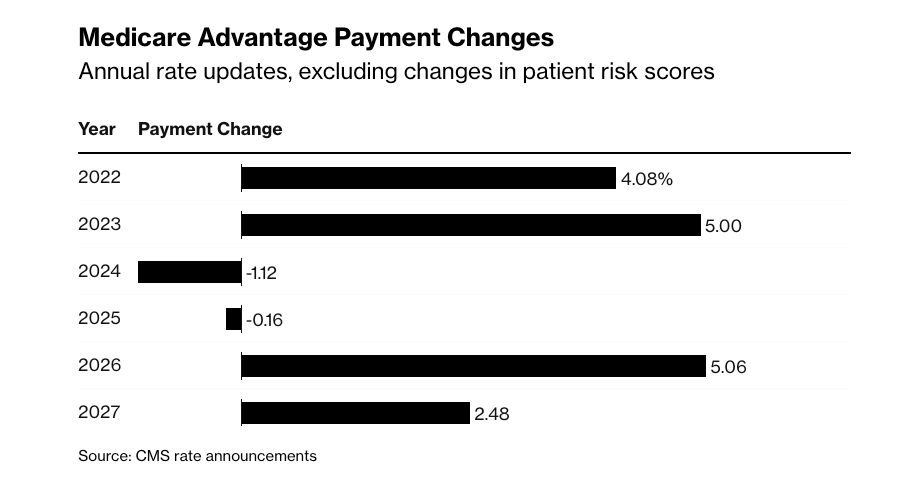

Three months ago, the Centers for Medicare and Medicaid Services proposed raising Medicare Advantage payment rates by 0.09% for 2027. That number, effectively flat, wiped out nearly $100 billion in market capitalisation across the largest health insurers in a single day. On Monday, CMS reversed course. The final rate came in at 2.48%, translating to more than $13 billion in additional federal payments to Medicare Advantage plans next year. As a result, UnitedHealth jumped roughly 9% in after-hours trading, Humana surged 12%, and CVS Health rose more than 8%. By Tuesday premarket, Humana was the best-performing stock in the S&P 500. A separate change to how CMS calculates risk-adjustment payments added another 2.5 percentage points, bringing the total effective increase closer to 5%. One investment firm estimated the true figure at 3.5% to 4% even before that adjustment, calling it a clean win for the industry. Analysts at RBC Capital Markets said the outcome was meaningfully above their base case of 1% to 1.5%. The bigger relief came from what CMS chose not to do. The agency delayed a planned recalibration of its risk-adjustment model, a system that ties insurer payments to how sick their enrolled populations are. Insurers had lobbied hard against the change, warning it would distort payments and accelerate market exits. Pausing it signals the administration is willing to pull back when the industry pushes back hard enough. CMS did follow through on one enforcement measure. Insurers will no longer be reimbursed for diagnoses documented through chart reviews unless the patient actually received treatment for those conditions. The practice, known as unlinked chart reviews, has drawn sustained criticism from government watchdogs for inflating risk scores and extracting higher payments without delivering additional care. The political calculus here is straightforward. Medicare Advantage now covers roughly 35 million Americans, more than half of all Medicare-eligible beneficiaries. Insurers had warned that inadequate rates would force them to cut benefits or exit less profitable markets. With midterms approaching, CMS had little appetite for that kind of disruption. The industry lobbied for 4% to 5%. It got something close enough. |

SpaceX Is Going Public

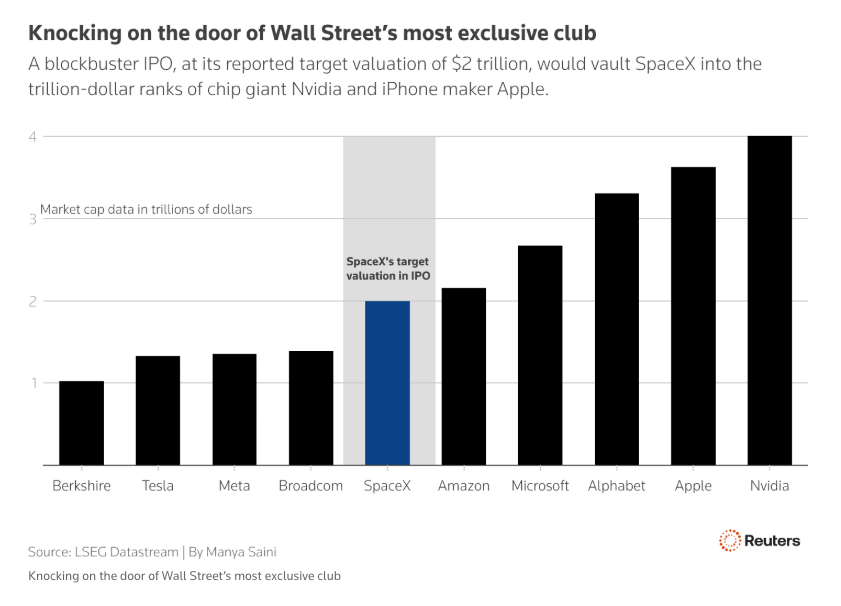

SpaceX has confidentially filed for an IPO that could raise up to $75 billion, shattering Saudi Aramco's $29.4 billion listing from 2019 as the largest in history. The targeted valuation sits at $1.75 to $2 trillion. For context, that would make SpaceX larger than every S&P 500 company except Nvidia, Apple, Alphabet, Microsoft, and Amazon, despite generating a fraction of their revenue. The roadshow is scheduled to launch the week of June 8, with the public prospectus expected in late May. 21 banks are involved, with Morgan Stanley, Bank of America, Citigroup, JPMorgan and Goldman Sachs as lead bookrunners. To secure their roles, those banks have been required to purchase Grok subscriptions worth tens of millions of dollars, the AI chatbot owned by xAI, which merged with SpaceX in February. The retail angle is unusual. SpaceX CFO Bret Johnsen told the bank syndicate that retail participation will be a bigger share of the offering than any IPO in history, with Musk reportedly targeting up to 30% for smaller investors against the industry standard of 5% to 10%. SpaceX is also planning to host 1,500 retail investors at a dedicated event on June 11, with participation open to investors across the US, UK, EU, Australia, Canada, Japan, and Korea. The fundamentals are a different story. Bloomberg Intelligence estimates SpaceX's rocket and Starlink businesses will generate close to $20 billion in revenue in 2026, with xAI contributing less than $1 billion. A $2 trillion valuation implies a price-to-sales ratio above 100 times, well above Palantir's 79 times, the current high in the S&P 500. One analyst put it plainly: "The juice has been squeezed from this orange." The xAI acquisition complicates the pitch further. The AI division is burning roughly $1 billion per month on computing infrastructure. Investors expecting a pure-play space company now carry significant AI exposure, in a crowded field where SpaceX has no obvious edge. What SpaceX does have is Starlink, a cash-generating satellite internet business with 9 million subscribers and growing defense contracts, and Musk's track record with Tesla shareholders. The valuation will be tested in two rocket launches expected before the June debut. If either fails, the IPO itself may not proceed. That alone tells you how much of this is still riding on physics, as opposed to finance. |

Tesla Is Down 22% This Year. The Bulls and Bears Are Miles ApartTesla delivered 358,023 vehicles in the first quarter of 2026, missing Wall Street's consensus of around 366,000 and coming in 7% below JPMorgan's own forecast of 385,000. The stock dropped 5.4% on the news and has now fallen for seven consecutive weeks, leaving shares down 22% year-to-date despite still being up roughly 51% over the past twelve months. The delivery miss is only part of the problem. Tesla produced 50,363 more vehicles than it sold in Q1, the largest inventory build in any quarter on record. Unsold inventory ties up cash, and that pressure is arriving at an awkward moment. Tesla is not expected to generate positive free cash flow this year, with capital expenditure rising to roughly $20 billion from $8.5 billion in 2025, as the company pours money into AI and robotics. JPMorgan analyst Ryan Brinkman reiterated an Underweight rating and a $145 price target, implying roughly 60% downside from current levels. His note pointed to a striking structural divergence: Tesla's production has grown 80% since Q1 2023, but the company is selling 15% fewer cars over the same period. Delivery volumes peaked in mid-2022. The stock, despite recent declines, is still up 50% from that point. The bull case rests almost entirely on what Tesla hasn't yet delivered. Morgan Stanley analyst Andrew Percoco called the unsupervised robo-taxi fleet the most important catalyst for the stock this year. Tesla launched its AI-trained robo-taxi service in Austin in June 2025 and planned to expand to nine cities in the first half of 2026. Investors are still waiting. ARK Invest's Cathie Wood, one of Tesla's most vocal supporters, bought around 40,000 shares across three funds on Monday, maintaining a price target of $2,600 by 2029. With SpaceX targeting a valuation of up to $1.75 trillion and planning an unusually large retail allocation, investors who have backed Tesla as a proxy for Musk's broader vision may find a more direct way to express that bet. Tesla's price-to-earnings multiple sits around 320. Whatever SpaceX's financials show when the prospectus goes public in late May, the comparison will not be flattering for the EV maker. |

That’s all for today!/