Hi there!

Welcome to FinSoar. I promise we’d take a look at what the future might bring, and here we are. GDP, Jobs, the S&P 500, and more:

2026: The Year GDP and Jobs Finally Decouple

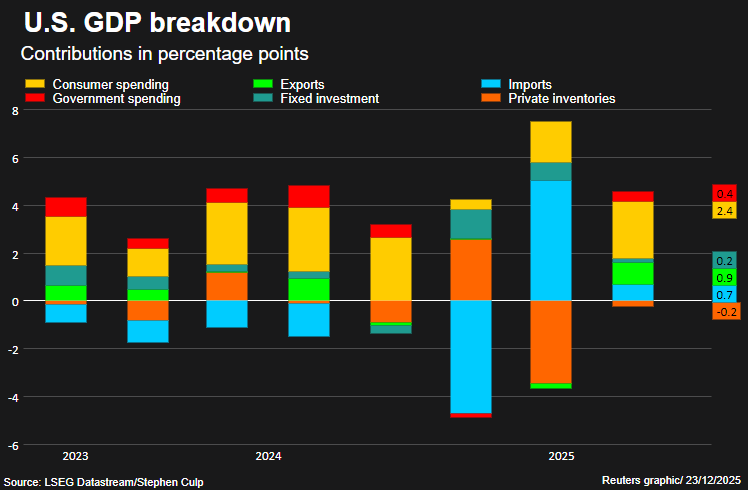

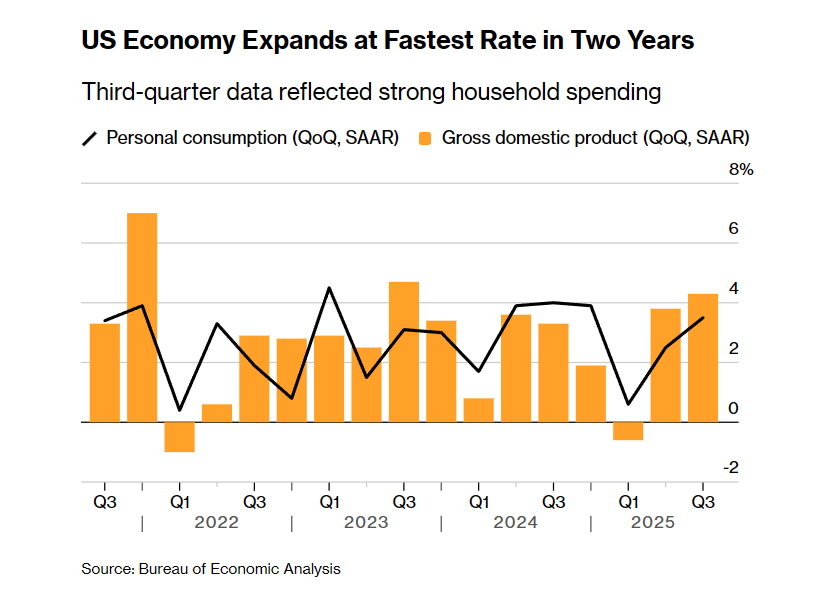

The economy enters 2026 with momentum but a fundamental contradiction. Q3 2025 GDP surged 4.3%, the fastest pace in two years. Yet unemployment climbed to 4.6%, the highest since 2021. Welcome to the jobless boom. Goldman Sachs predicts US GDP will accelerate to 2.6% in 2026, above the 2% consensus. Global growth is forecast at 2.8%. Three forces will drive this: reduced tariff drag as duties stabilize, $100 billion in extra tax refunds in the first half from Trump's One Big Beautiful Bill Act, and easier financial conditions. But Goldman sees the unemployment rate stabilizing around 4.5%, with no meaningful decline anytime soon. At a gathering of CEOs in Manhattan, 66% said they planned to either fire workers or maintain existing headcount. Only a third indicated hiring plans. "You're going to see a lot of wait and see," said Chris Layden, CEO of staffing company Kelly Services. "Some of the looming uncertainty will mean that we're going to continue to see an investment in capital over people." Fed governor Christopher Waller said at the Yale summit: "When I go around and talk to CEOs, everybody's telling me, 'Look, we're not hiring because we're waiting to try to figure out what happens with AI.'" "Everybody's afraid for their jobs. I'm dead serious," Waller added. JPMorgan predicts "uncomfortably slow growth" in the labor market in the first half of 2026, with unemployment peaking at 4.5%.

The bank blames Trump's immigration crackdown reducing labor supply, an aging population, and AI driving productivity without jobs. The monthly job gains needed to keep unemployment steady could tumble to just 15,000 from 50,000. Goldman's Jan Hatzius warns the weakness in the job market for college-educated workers is particularly notable. Unemployment for college graduates aged 25 or older stood at 2.8%, about 50% higher than its 2022 low. For those aged 20-24, it climbed to 8.5%, up 70%. College graduates account for more than 40% of the US labor force and 55-60% of labor income. AI companies may invest more than $500 billion in 2026. Consensus estimates for hyperscaler capex climbed to $527 billion, up from $465 billion at the start of Q3 earnings season. But Goldman notes consensus estimates have proven too low for two years running. Historical technology cycles suggest as much as $200 billion upside to current estimates. The Fed is expected to pause rate cuts in January before delivering cuts in March and June, pushing the funds rate to 3-3.25%. Trump is expected to nominate a new Fed chair who supports lower rates, with Kevin Hassett currently the most likely nominee. Wall Street remains bullish on stocks despite elevated valuations. Bank of America targets 7,100 for the S&P 500, JPMorgan and HSBC target 7,500, and Deutsche Bank targets 8,000, implying 3-16% gains. S&P 500 earnings are expected to grow 15% in 2026, up from 13% in 2025. Kristy Akullian at BlackRock says: "We are still pretty optimistic. We're pretty upbeat, relatively bullish." Ryan Detrick at Carson Group expects 12-15% gains, noting: "We simply don't see a recession next year. And when you don't have a recession, the S&P 500 is up double-digits almost 70% of the time".

But risks loom. Inflation might be the biggest spoiler. If core inflation rises to 4%, the Fed will have to raise rates again. Jeffrey Buchbinder at LPL Financial says: "AI disappointment is the No. 1 risk to the market in 2026". The delayed impact of tariffs presents another threat. Economist Jeffrey Frankel notes that companies have absorbed much of the tariff costs so far but won't let them erode margins indefinitely. Assuming tariffs remain, the US can look forward to more price increases and downward pressure on real incomes in 2026. Mortgage rates are expected to hover around 6.3% in 2026, down from 6.6% in 2025 but unlikely to dip below 6% for any meaningful period. Home price growth will slow to around 1% versus wage growth of 4%, the first sustained period of home prices growing slower than wages since the financial crisis. Refinance volume is expected to surge more than 30% to $670 billion. The contradictions are stark. Strong growth meets stagnant jobs. Massive AI investment creates little employment. Robust earnings fail to translate to hiring. JPMorgan expects this disconnect to reverse in the second half as tax cuts, consistent tariff policy, and Fed cuts take hold. Goldman's forecast depends on tariffs remaining stable. If Trump escalates trade conflicts again, all bets are off. The full tariff pass-through to consumers that hasn't happened yet could materialize with force. 2026 is shaping up to be the year where old rules don't matter. Economic growth without jobs. AI spending without productivity gains. Corporate profits without hiring. The disconnect can't last forever. Something has to give. |

That’s all for today!