Welcome to another weekend with FinSoar! Today I’m looking at S&P 500 maintaining regulations in the face of an early SpaceX IPO, even more Trump tariffs under the guise of “forced labor” and a case study stock: Lululemon.

SpaceX Loses Its Bid for Fast-Track S&P 500 Entry

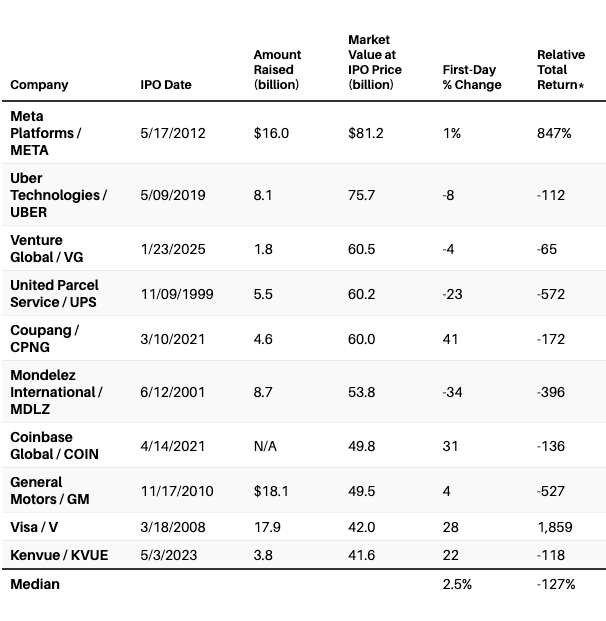

S&P Global said on Thursday it would not change the entry requirements for its major indices, effectively blocking Elon Musk's SpaceX from a swift entry into the benchmark S&P 500 ahead of the world's biggest-ever IPO. The decision means SpaceX, which is raising $75 billion at a targeted $1.75 trillion valuation, cannot bypass the index's profitability rule. To join the S&P 500, a company must be profitable under GAAP in its most recent quarter and across its most recent four quarters combined. SpaceX posted a net loss of $4.94 billion in 2025, even as revenue rose 33% to $18.67 billion. S&P said "exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization." The decision followed investor consultations in which S&P had considered shortening the listing seasoning period, waiving minimum float requirements, and removing its profitability requirement. It declined to change any of them. The Nasdaq took the opposite approach. It has already changed its rules to make it easier for SpaceX, Anthropic, and other newly listed megacaps to join the Nasdaq 100. Nasdaq 100 index funds will be forced to buy a sizeable portion of publicly available SpaceX shares when the company joins. That divergence sets up the central risk for retail buyers — the Nasdaq's fast-track approach has raised concerns that new retail investors could become "the cash cow of exit liquidity for legacy SpaceX shareholders." SpaceX is not entirely shut out of indexing. S&P said it would modify entry rules for its broader S&P Total Market Index and Dow Jones US Total Stock Market Index, creating a pathway to those less widely followed indexes. The company has also become eligible for the Russell US Equity Indexes and the FTSE Global Equity Index Series. The historical record argues for patience. Of the 36 US companies that went public at a market cap of $15 billion or more, only nine have beaten the S&P 500 from their first-day closing price. Since 1980, issuers with a price-to-sales ratio above 40 have seen an average three-year drop of 45% from their first day's close. At a $1.8 trillion valuation, SpaceX would trade at 93 times trailing sales, even as it posted a $1.9 billion operating loss in Q1 2026. University of Florida professor Jay Ritter told Barron's that the one thing he is "certain about is the stock is going to be very volatile." The Meta comparison cuts both ways: those who bought at the IPO are up 1,474%, but those who waited six months are up 2,454%.

|

Trump Revives His Tariffs Under a Forced-Labor BannerThe Trump administration proposed new tariffs of 10% to 12.5% on imports from 60 trading partners on Tuesday, accusing them of failing to curb trade in goods made with forced labor. The plan from the US Trade Representative's office comes from a Section 301 unfair trade practices investigation designed to help rebuild Trump's emergency tariffs, which the Supreme Court struck down in February. The legal context is the real story. After the Supreme Court ruled Trump's "Liberation Day" tariffs illegal, he imposed 10% across-the-board duties. A specialized trade court then ruled those also unlawful last month, though they remain in place during appeal. The temporary 10% levies expire July 24. The forced-labor tariffs would let Trump skirt those court-imposed limits using a different legal authority. The structure splits the 60 partners into two tiers. The USTR proposed 10% additional duties on Canada, the EU, Britain, Mexico, Taiwan, Indonesia, Pakistan, and others. The remaining 45 countries, including China, India, Japan, South Korea, Vietnam, and Australia, would face 12.5%. The 60 partners listed account for almost all goods sold to the US. The proposal is subject to public comment through July 6, with a hearing on July 7. Trading partners pushed back hard. The European Commission called the tariffs "unjustified" and reiterated its commitment to the 15% tariff deal it agreed with Washington last July. Bernd Lange, chair of the European Parliament's trade committee, called the findings "utterly absurd" given a 2024 EU law banning forced-labor imports, adding that "a tariff measure is sought first, and only then is a suitable legal justification found." China denied forced labor exists within its borders. India called it a pressure tactic. The exemptions tell their own story. The USTR exempted energy, rare earths, beef, coffee, certain fruits and vegetables, pharmaceuticals, and aircraft parts — revealing sensitivities over the cost-of-living hit to consumers. Human Rights Watch's Hélène de Rengerve warned the measure "might even be counterproductive to the objective of fighting forced labour." For trading partners who spent a year building trust with Washington, the message is that the tariff wall is going back up, with a new justification bolted on each time the courts knock the last one down. |

Lululemon Cuts Its Outlook as the Turnaround Stalls

Lululemon shares fell 12% on Friday after the athletic apparel maker cut its full-year guidance and issued a weak current-quarter outlook, deepening concerns about its turnaround. The stock was on track to lose more than $1.7 billion from its $14.44 billion market value. Lululemon shares have lost nearly 63% of their value over the past 12 months. The quarter itself beat lowered expectations. Lululemon posted Q1 revenue of $2.47 billion against $2.43 billion expected, with revenue up 4% year over year and comparable sales growing 1%. But net income fell to $195 million, or $1.69 per share, down from $314.6 million, or $2.60 per share, a year earlier. The problem is geographic. Lululemon's growth came almost entirely from abroad. International sales grew 22% and international comparable sales rose 13%. Meanwhile, the Americas — its largest and most important region — saw sales decline 3% and comparable sales fall 5%, marking the fifth straight quarter of declines in the market. The guidance cut is what spooked investors. Lululemon now expects full-year sales of $11 billion to $11.15 billion, down from a prior range of $11.35 billion to $11.50 billion. It cut full-year EPS guidance to $10.95-$11.15 from $12.10-$12.30, more than a dollar below analyst expectations. Current-quarter EPS guidance came in well below the $2.68 Wall Street expected. Interim CEO Meghan Frank blamed "spikes of negative commentary in the media" tied to the proxy fight with founder Chip Wilson and product launches that failed to generate the anticipated response. Profitability is the deeper wound. Gross margin fell 4.1 percentage points to 54.2%, driven primarily by tariffs, which hit margins by 2.8 points, and discounting. With fewer shoppers, the company has leaned on discounting, hurting both margins and its premium brand reputation. Barclays analysts said Lululemon has "entered the 'trap' phase, where fundamentals are deteriorating" as competition stiffens and pricing power fades on core franchises. Newcomers like Alo Yoga and Vuori are taking share. Lululemon hired Nike veteran Heidi O'Neill as its next CEO and settled the Wilson proxy fight in May, granting Wilson two board seats in exchange for his silence. But O'Neill does not start until September, leaving interim leadership in place and the real strategic reset months away. Jefferies analysts said "a full strategic reset under the new CEO is required." For now, investors are stuck waiting on a turnaround that has not yet found its footing, in a brand losing pricing power in the one market that matters most. |

That’s all for today!/