Welcome to FinSoar! This weekend I’m looking at treasury yields, depressing consumer sentiment and beauty companies butting heads:

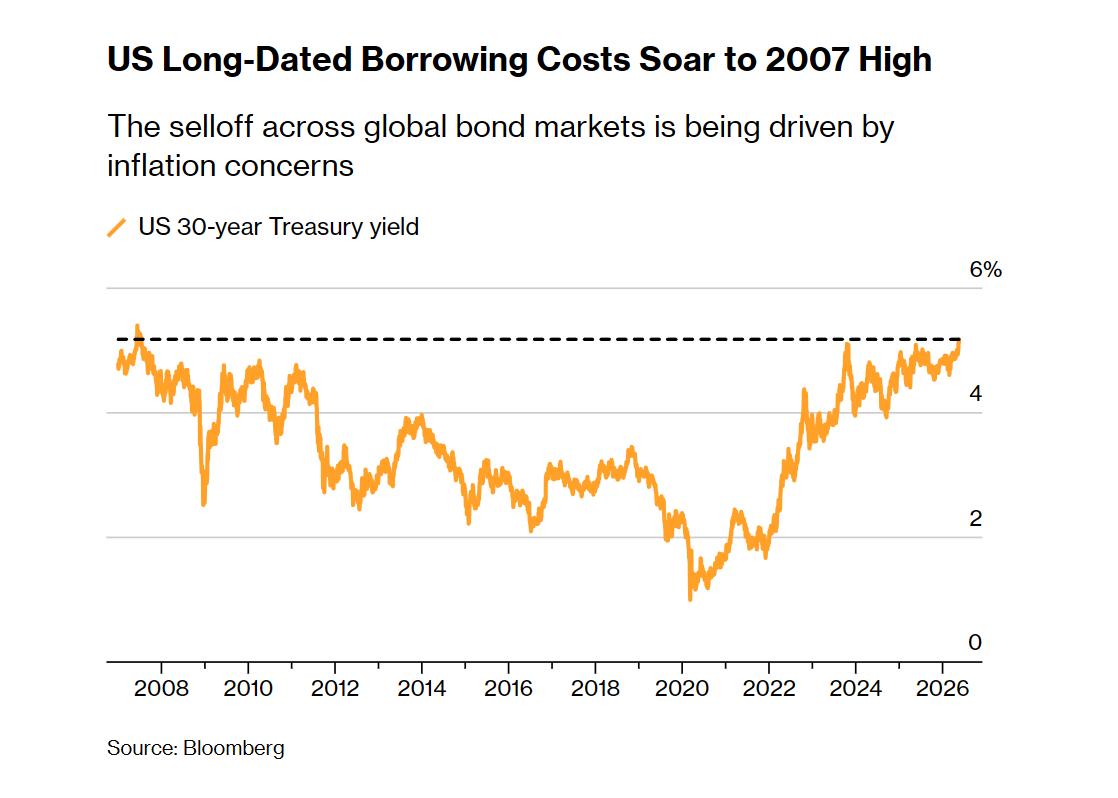

The 30-Year Treasury Yield Hits a 2007 High

The US 30-year Treasury yield rose to 5.20% Tuesday, the highest level since June 2007 on the eve of the global financial crisis, as a global bond market selloff deepened on inflation and fiscal concerns. The benchmark 10-year yield climbed to 4.69%, its highest since January 2025, per Bloomberg. The selloff was not driven by a fresh oil spike or single catalyst — it reflects a broader repricing of long-end debt. The April CPI print at 3.8% pushed traders to price in an 80% probability of a 25bp Fed hike by year-end, per overnight index swaps. That is a complete reversal from late February when markets were pricing in three Fed cuts in 2026. CME Group's FedWatch tool now puts combined odds of a Fed hike by December at 59.1%. The fiscal dimension is also driving the move. The US national debt stood at $38.9 trillion as of May 15, up $2.7 trillion in the last year. The median budget deficit estimate from primary dealers shows a $1.95 trillion gap for the year ending September, widening to $2 trillion in 2027. A mid-May 30-year Treasury auction cleared above 5% for the first time since 2007, with demand described as unremarkable. Barclays global research chairman Ajay Rajadhyaksha told Bloomberg that "with debt rising faster than growth, worsening inflation profiles, and no political will for fiscal reform, there is little reason to reach for the long end." The mechanical pressure has become self-reinforcing. Mortgage-backed securities investors have been forced into convexity hedging, selling Treasury futures to manage duration risk as rates climb. Morgan Stanley Investment Management's Vishal Khanduja told Reuters that "the velocity of the move in yields has been concerning and we have seen some forced selling because of convexity hedging." Barclays' Amrut Nashikkar said the MBS market now holds more than $2 trillion of mortgages with coupons of 5% or higher, making hedging activity "more destabilizing for rates markets" than in 2023. HSBC told clients US Treasuries are "firmly in the Danger Zone" where 10-year yields pressure all asset classes. A Bank of America survey published Tuesday found 62% of global hedge fund managers expect 30-year yields to hit 6%. Barclays and Citigroup strategists have flagged 5.5% as the next risk level. BMO Capital Markets' Ian Lyngen told Bloomberg that if 30-year yields reach 5.25%, "there will be a more durable pullback in equity valuations." For now, the bond market is doing the work the Fed has not — tightening financial conditions through mortgage rates, corporate borrowing costs, and the cost of refinancing the federal deficit. |

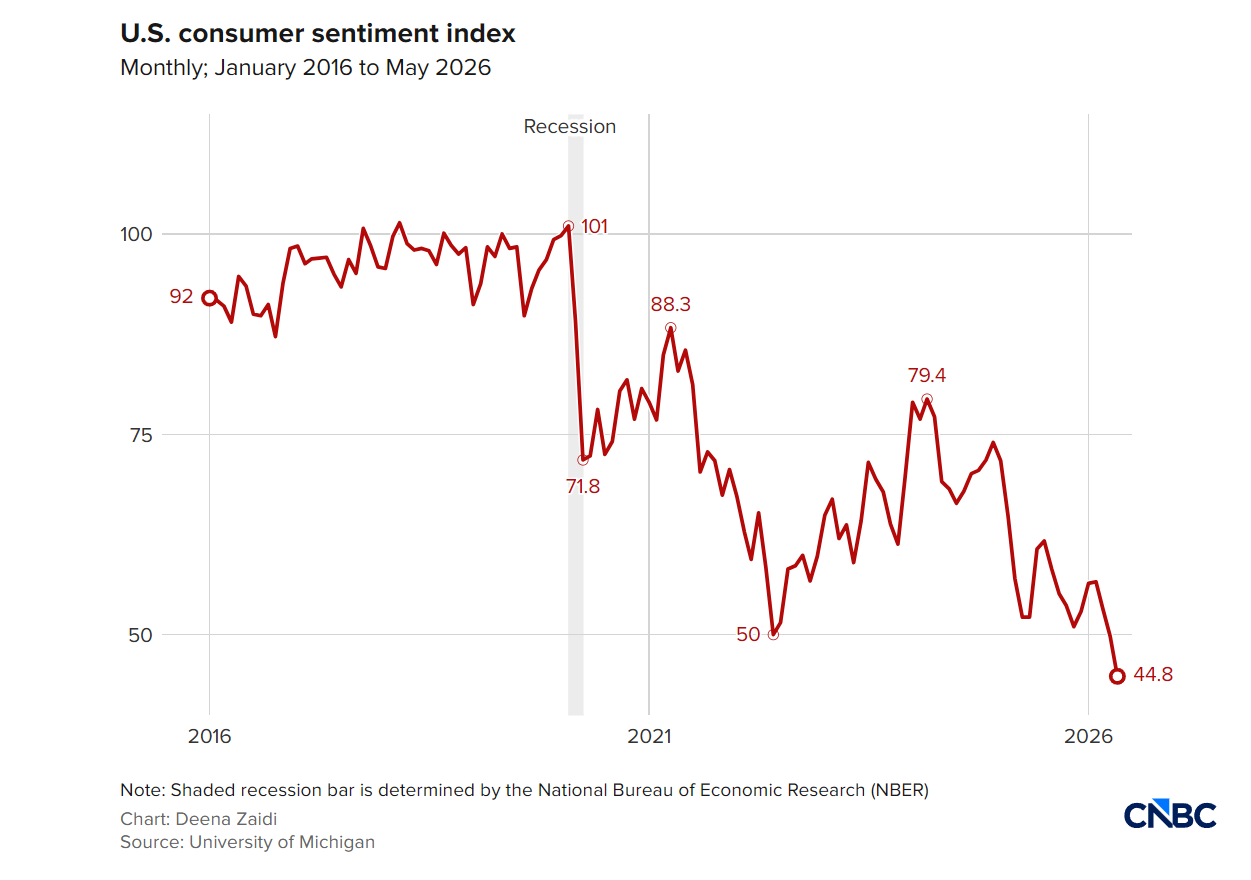

US Consumer Sentiment Hits a Record Low

US consumer sentiment fell to an all-time low in May, with the University of Michigan's Surveys of Consumers index dropping to a final reading of 44.8, down from 49.8 in April and below the preliminary reading of 48.2. Per Reuters, economists polled had forecast the index unchanged at 48.2. This marks the third straight monthly decline. Americans are now feeling worse than they did during wars, the 1970s oil crisis, 9/11, the Great Recession, the Covid-19 pandemic, and the post-pandemic inflation surge, according to CNN. The driver is straightforward. The Iran war is now in its third month, the Strait of Hormuz has been effectively choked off, and the national average retail gasoline price has jumped more than 50% since the war started to about $4.552 a gallon per AAA data cited by Reuters. Surveys of Consumers Director Joanne Hsu noted that "57% of consumers spontaneously mentioning that high prices were eroding their personal finances, up from 50% last month." The sharpest declines came from lower-income consumers and those without college degrees, groups disproportionately hit by fuel and food costs. Sentiment among Republicans and Independents dropped to the lowest level of Trump's second term. A Reuters/Ipsos poll this week showed Trump's approval rating near its lowest level since he returned to the White House, hit by a drop in support among Republicans. The growing discontent is a real risk to GOP majorities heading into November midterms, per Reuters. The Fed implications are what should worry policymakers most. Inflation expectations are unanchoring. The survey's measure of expected inflation over the next year rose to 4.8% from 4.7% in April. Long-run expectations over five years shot up to 3.9% from 3.5%, per CNBC. Republicans' long-run inflation expectations are now more than double their February 2025 monthly reading. Fed Governor Christopher Waller said in a speech Friday that "some expectations from one to five years ahead have moved up since the beginning of 2026, which I find concerning." The disconnect between sentiment and asset markets is stark. The Dow Jones Industrial Average hit a record high Friday for the first time since the Iran war began. Rising stock prices are not cheering consumers because most household wealth is locked in retirement accounts that cannot be drawn down for daily expenses. Economist Christopher Rupkey told CNN the "American consumer is treading water here, and the income tax refunds must be gone already or the money spent on the higher prices seen everywhere in the economy." |

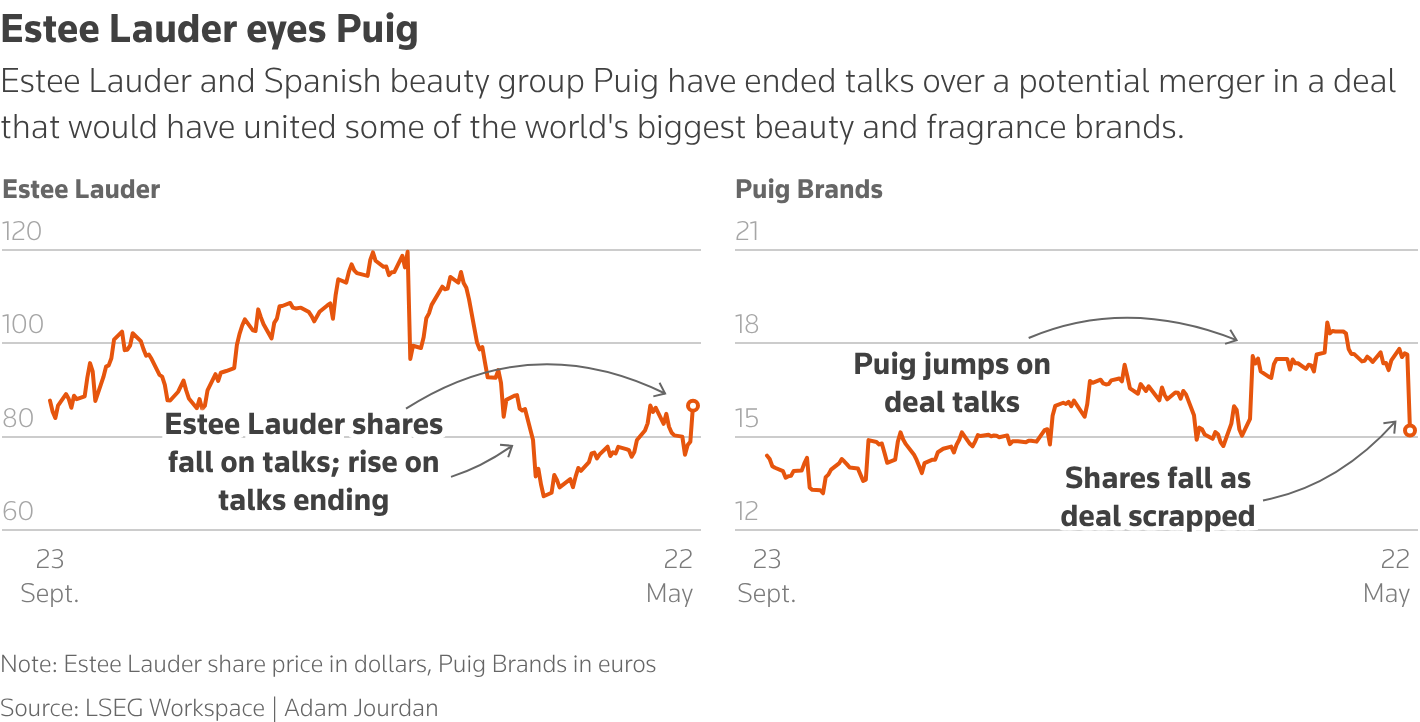

The Death of a $40 Billion Beauty Deal

Estée Lauder and Spanish beauty group Puig terminated merger talks Thursday night, ending a potential $40 billion combination that would have brought brands including Clinique, Tom Ford Beauty, Carolina Herrera, and Charlotte Tilbury under one roof. Estée Lauder shares jumped 11% Friday, while Puig fell roughly 14% in Madrid, per CNBC. The sticking point was Charlotte Tilbury herself. The British makeup entrepreneur sold a controlling stake in her eponymous brand to Puig for over $1 billion in 2020, retaining a minority position. The deal with Estée Lauder would have triggered a change of control clause allowing Tilbury to potentially sell her stake, according to the Guardian. Tilbury inserted herself into the negotiations and pushed for a renegotiation of her buyout terms, per the Wall Street Journal. Her demands "would have materially affected the transaction's economics." Reuters reported that on Thursday evening in Barcelona, Marc Puig got on the phone with Estée Lauder chairman William Lauder to assess the deteriorating situation. Shortly afterward, advisers on both sides exchanged messages, with one including a skull emoji to signal the deal was dead. The two sides had repeatedly been on the verge of announcing a merger over months of meetings in Paris, New York, and Barcelona. Investor reaction tells the story. Estée Lauder shares had slumped roughly 20% since the talks became public in March, with the Lauder family controlling more than 80% of voting power despite owning about 38% of shares per the Guardian. Friday's market reaction reversed those positions, with Estée Lauder up 11% and Puig down 14% per Barron's. AJ Bell's Dan Coatsworth told CNBC the termination was a near "lucky escape" for Estée Lauder investors, calling the proposed combination "a bit like a jumble sale rather than a match made in heaven." Estée Lauder now refocuses on its "Beauty Reimagined" turnaround plan. The company already expects a $100 million hit to full-year profitability from tariffs and has laid out plans to cut up to 10,000 positions in pursuit of $1.2 billion in cost savings, per CNBC. Tilbury, who topped last year's Sunday Times beauty rich list with an estimated £350 million fortune, demonstrated the leverage a brand-defining personality holds when their economics get renegotiated mid-deal. For Wall Street, the lesson is to price founder optionality into beauty M&A. For Estée Lauder, the lesson is that Plan A still needs to work. |

That’s all for today!/