Welcome to another intriguing weekend read! I’m looking at the President’s dubious monetization of social media for Wall Street Firms, falling Netflix shares, and a lowball offer for PayPal:

Truth Social Will Sell Traders Faster Access to Trump's Posts

Trump Media wants to sell Wall Street firms millisecond-faster access to Truth Social posts, monetizing a president whose social media activity routinely moves stocks and oil. The product, Truth API, launches August 1 for institutional customers and delivers a real-time feed from the platform's top 10 accounts. Some buyers have already signed up. The feed is geared toward algorithmic and high-frequency trading firms, where an edge of milliseconds carries real value. Trump Media has not disclosed pricing or how much faster subscribers will see posts than everyone else. The underlying asset is essentially one account. Trump has 12.9 million followers and posts sometimes more than 100 times a day, using the platform to announce policy on tariffs, the Fed, and the Iran war. His Hormuz posts have battered oil futures, leaving traders on the wrong side of million-dollar bets. The company was blunt about the pitch. "Markets already move on Truth Social posts," interim CEO Kevin McGurn said, calling the API a high-margin, recurring revenue stream built on proprietary assets. Other platforms including X and Reddit sell similar feeds. Trump owns about 41% of Trump Media through a revocable trust managed by Donald Trump Jr., a stake worth more than $1 billion. Presidents have traditionally divested holdings posing conflicts. Trump has kept his media, crypto, and real estate interests intact. Former SEC lawyer Tyler Gellasch told the NYT there is little doubt about demand, but the rules around charging for faster access to a government official's statements are unclear. Trump Media shares closed at $9.28 Thursday, down 77% since Trump retook office and nearly 85% from March 2024. The unprofitable company has branched into streaming, crypto, and a pending nuclear fusion merger while struggling to generate revenue. Truth Social has never found an audience beyond one man's megaphone. Trump Media has now decided to sell the megaphone by the millisecond. |

Netflix Cuts Back on Viewing Data Right as Wall Street Starts Asking

Netflix turned in a fine quarter and then told investors it would show them less of the one number they cared about. So the stock fell 9%. Revenue of $12.56 billion came in just under the $12.58 billion consensus, while earnings of 80 cents beat by a penny. Netflix sees $12.86 billion and 82 cents next quarter against Wall Street's $13 billion and 84 cents. Then came the disclosure change. Netflix publishes a viewing report called "What We Watched" twice a year. From 2027, it goes annual. The company says the goal is to keep the focus on revenue and operating profit. It already stopped publishing quarterly subscriber numbers in 2025. Timing is everything, and this timing is bad. Global viewing hours rose 2% in the first half to 97 billion, up from 96 billion in the back half of 2025 and about 95 billion a year earlier. Growth, technically. Thin enough to invite questions. Management's defence is that hours are the wrong lens. "All hours are not created equal," co-CEO Greg Peters said on the call. Live sport proves the point: more than 5% of content spend, roughly 1% of viewing hours, yet six of the ten biggest sign-up days in five years. If engagement is healthy, investors should want more visibility, not less. Some think the panic is overdone. Morgan Stanley's media team wrote that investors are overly focused on the headline hours number, which correlates less with revenue than feared. They may be right. Netflix has a 2% cancellation rate, an industry low, and still leads paid streamers on US TV time. Meanwhile YouTube, TikTok, and Instagram absorb the attention that used to be Netflix's by default. The stock had already dropped 31% since April's report. |

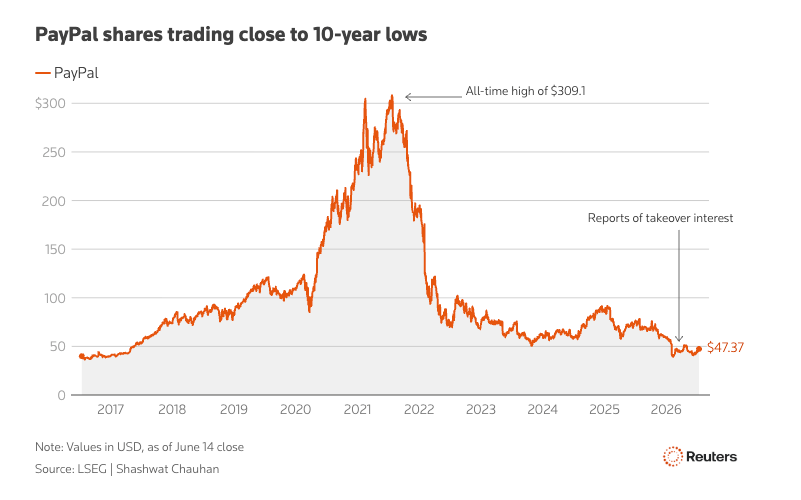

Stripe Offers Cheap Bid for PayPal

Stripe and Advent International want to buy PayPal for $60.50 a share, about $53 billion. PayPal jumped 17% in response, but analysts spent the day arguing the number was too low. The offer went in earlier this month with roughly $50 billion in committed bank financing, a 28% premium to Tuesday's close. Stripe, Advent, and Block are putting in $17 billion of equity, and PayPal's board was set to meet as soon as July 20. Stripe and Advent would each own half, with no plan to break the company up. The premium looks generous against yesterday. Against history, less so. PayPal peaked above $300 a share in 2021 at a market value north of $280 billion. It has fallen 24% in the past year alone. The strategic logic is clear. Stripe sells to merchants. PayPal brings just under 440 million active accounts, the Venmo network, and the checkout button consumers already recognise. Stripe's own consumer arm, Link, has more than 250 million users. Together, the two would process roughly $3.7 trillion a year, enough volume to route more payments across their own rails and lean less on Visa and Mastercard. Sellers rarely love being caught mid-repair. Enrique Lores took over in March, split PayPal into three units, and promised $1.5 billion in savings over two to three years. He has been in the job four months. A bid arriving now values the turnaround at zero. William Blair's Andrew Jeffrey thinks $70 is available if this is an opening salvo. Great Hill Capital's Thomas Hayes went further, arguing even above $80 would discount the free cash flow. Deutsche Bank's read was broader: deal or no deal, this portends continued consolidation in payments. PayPal invented the consumer side of online payments and got outrun on it. Stripe, valued privately at $159 billion, is offering a third of that to finish the job. |

That’s all for today!/